97% of executives deployed AI agents in the past year. 80% of organizations say those agents are already delivering measurable ROI.

88% of executives say agentic AI will increase AI-related budgets in the next 12 months, while 79% say AI agents are already being adopted in their companies.

That is why AI agents are being tracked so closely in 2026: adoption is already broad, but the real question is whether organizations can scale agents into durable workflows without losing control of governance, integration, or ROI.

This article breaks down the market size, adoption curve, use cases, productivity, security risk, coding, geography, and the 2026 outlook.

AI Agents Statistics: Key Insights & Takeaways

- 97% of executives say their company deployed AI agents in the past year, while 52% of employees are already using them, highlighting how quickly AI agents have entered mainstream enterprise workflows.

- 80% of organizations report measurable economic returns from AI agents, but only 23% say those agents have delivered significant ROI, revealing a substantial gap between productivity gains and realized business value.

- 88% of executives plan to increase AI budgets in the next 12 months because of agentic AI, and 79% say AI agents are already being adopted within their organizations.

- 51% of organizations already have AI agents in production, while 78% have active plans to deploy them, showing that the market is rapidly moving from experimentation to operational deployment.

- Over 40% of agentic AI projects could be canceled by the end of 2027, according to Gartner, making execution risk one of the biggest challenges facing the industry.

- 67% of executives believe their company has already experienced a data leak or security incident related to unapproved AI tools, while 36% have no formal plan to supervise AI agents.

AI Agents Statistics At A Glance

| Metric | Figure |

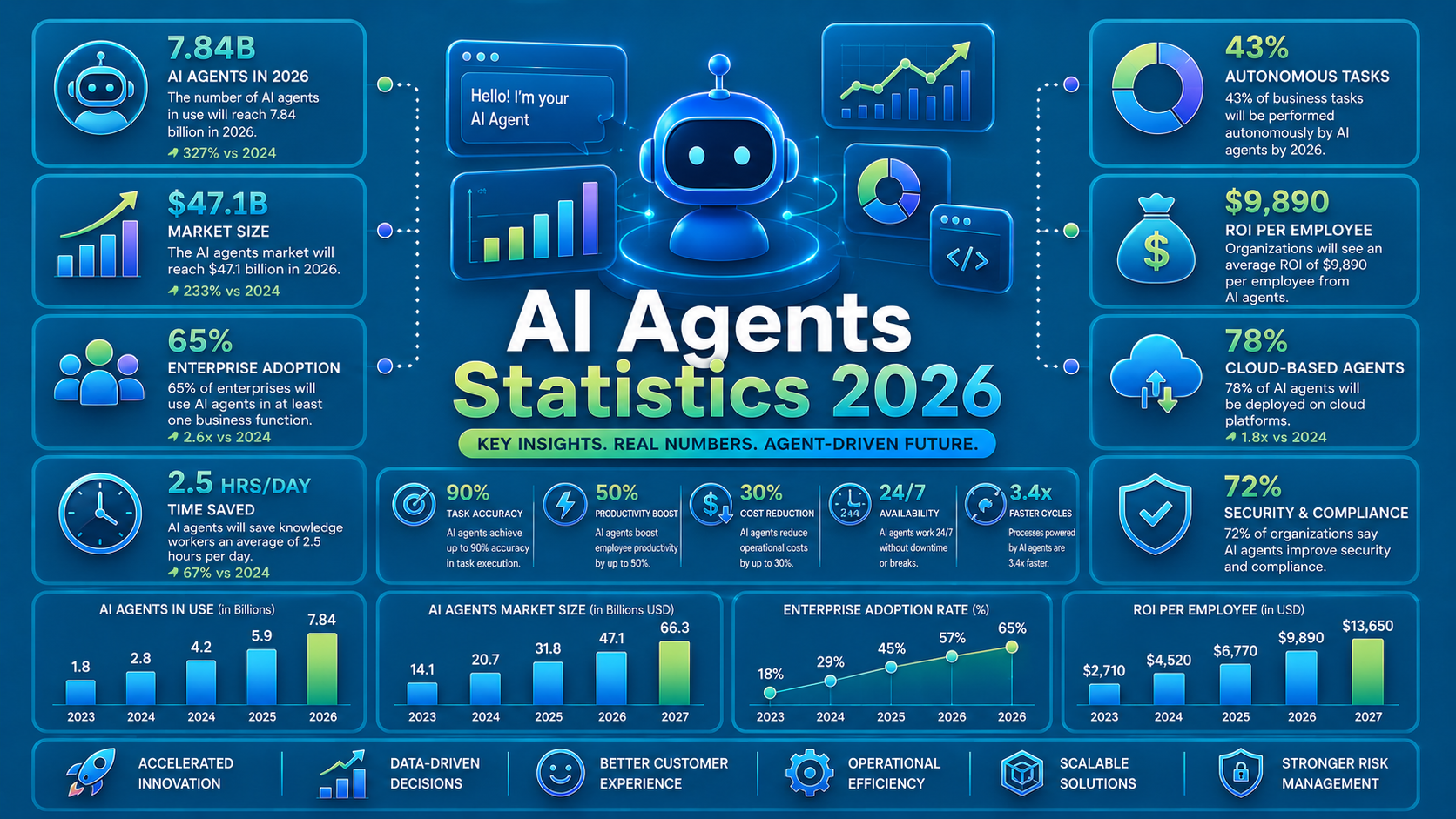

| Market size (2025) | $7.84B |

| Market size (2026) | $11.47B |

| Projected market size (2030) | $52.62B |

| CAGR | 46.3% |

| Enterprise adoption rate | 79% of companies adopting AI agents |

| Workforce using AI agents | 52% of employees |

| Orgs with agents in production | 51% |

| ROI satisfaction rate | 80% report measurable economic returns |

| Enterprise apps with agents | 33% by 2028 |

| Project cancellation risk rate | 40%+ by 2027 |

| Top geography | North America remains the largest market |

AI Agents Statistics 2026: Deep Dive

1. AI Agents Market Size & Growth Statistics

The AI agent market is growing fast, but forecasts differ because analysts do not all measure the same scope. MarketsandMarkets pegs the market at $7.84 billion in 2025 and $52.62 billion by 2030 at a 46.3% CAGR, while Grand View Research estimates $7.63 billion in 2025 and $182.97 billion by 2033 at a 49.6% CAGR.

The gap mostly reflects differences in how much orchestration, platform infrastructure, and adjacent agentic AI software is included in the category.

The broader market is not just about standalone agents. Gartner’s public forecast says 33% of enterprise software applications will incorporate agentic AI by 2028. Gartner also says 15% of day-to-day business decisions will be made autonomously by agentic AI by 2028.

The strongest growth signal inside the market is specialization. MarketsandMarkets says vertical AI agents are the fastest-growing segment, with a 62.7% CAGR through 2030, outpacing the overall market at 46.3% CAGR.

AI agent market size by year, 2024–2034

Derived projection note: all rows except 2025 are calculated from MarketsandMarkets’ published 2025 base of $7.84B and 46.3% CAGR. They are not separately published annual figures.

| Year | Market size (USD B) | Type |

| 2024 | 5.36 | Derived |

| 2025 | 7.84 | Published |

| 2026 | 11.47 | Derived |

| 2027 | 16.78 | Derived |

| 2028 | 24.55 | Derived |

| 2029 | 35.92 | Derived |

| 2030 | 52.55 | Derived |

| 2031 | 76.87 | Derived |

| 2032 | 112.47 | Derived |

| 2033 | 164.54 | Derived |

| 2034 | 240.72 | Derived |

Single-agent vs. multi-agent AI agent market share

MarketsandMarkets says multi-agent systems are the faster-growing architecture, while Azumo’s compiled market page reports 59.24% share for single-agent systems in 2025. That leaves 40.76% for multi-agent systems on a derived basis, which makes the 2026–2030 shift toward orchestration and coordination easier to see.

| Agents type | 2025 share / CAGR |

| Single-agent systems | 59.24% share |

| Multi-agent systems | 40.76% share, derived from single-agent share |

| Multi-agent systems | 48.5% CAGR |

| Vertical/domain-specific agents | 62.7% CAGR |

| Overall AI agents market | 46.3% CAGR |

2. AI Agents Adoption Statistics

Adoption is already beyond experimentation in many organizations. PwC says 79% of companies are already adopting AI agents, and 88% of executives plan to raise AI-related budgets because of agentic AI. WRITER adds that 97% of executives say their company deployed AI agents in the past year, while 52% of employees are already using them.

Production use is also real, not just aspirational. LangChain reports 51% of respondents have agents in production today, and 78% have active plans to put them into production soon. Anthropic’s 2026 report shows 57% using agents for multi-stage workflows and 16% already running them across cross-functional processes.

Read our complete report on Anthropic’s statistics here →

The gap is maturity, not awareness. WRITER says 79% of organizations face challenges adopting AI, and 59% are spending more than $1 million a year on AI technology, which helps explain why adoption keeps rising even as operational friction stays high.

Adoption stage breakdown

| Stage | Share of organizations | Source |

| Exploring | 21% still relying mainly on pre-built agents | Anthropic compilation |

| Piloting | 47% using a hybrid build / buy model | Anthropic compilation |

| Production | 51% already in production | LangChain |

| Scaling | 16% already cross-functional; 29% plan cross-functional deployment in 2026 | Anthropic |

| Adoption signal | Figure | Source |

| Executives deploying agents in the past year | 97% | WRITER |

| Employees already using agents | 52% | WRITER |

| Companies spending over $1M annually on AI | 59% | WRITER |

| Organizations planning more complex agent work in 2026 | 81% | Anthropic compilation |

3. AI Agents Use Case Statistics

The most common agent use cases are still knowledge-work heavy. LangChain found that research and summarization leads at 58%, followed by personal productivity and assistance at 53.5% and customer service at 45.8%. That pattern suggests agents are first winning where work is repetitive, text-heavy, and easy to route into measurable workflows.

Anthropic’s 2026 report shows the same direction, but with a stronger enterprise slant. It says data analysis and report generation reach 60%, internal process automation reaches 48%, and research and reporting is on the roadmap for 56% of organizations over the next year.

Anthropic also reports 59% for code generation, documentation, testing, and review, making software work one of the most valuable agent categories.

Sales and outreach are also emerging as meaningful use cases. Anthropic’s data on Claude API usage shows business sales and outreach automation rising, including lead qualification, customer enrichment, and cold-email drafting. That is one reason agent adoption is spreading beyond support teams and into revenue operations.

| Use case | Adoption / impact % | Primary industry / function | Source |

| Research & summarization | 58% | Knowledge work | LangChain |

| Personal productivity | 53.5% | Individual workflow automation | LangChain |

| Customer service | 45.8% | CX / support | LangChain |

| Data analysis & report generation | 60% | Analytics / operations | Anthropic |

| Internal process automation | 48% | Ops / back office | Anthropic |

| Research & reporting planned | 56% | Enterprise research | Anthropic |

| Code generation / testing / documentation | 59% | Software engineering | Anthropic |

| Sales & lead qualification | Rising as an API workflow | Revenue operations | Anthropic |

4. AI Agents Enterprise Adoption & Regional Readiness Statistics

Enterprise adoption is increasingly about capability planning, not just tool buying. PwC says 66% of organizations adopting AI agents say they are already seeing measurable productivity gains, and 88% of executives plan to increase AI-related budgets because of agentic AI.

India is the clearest country-level acceleration story in the current data set. Microsoft says 93% of Indian business leaders intend to use AI agents to extend workforce capabilities within 12–18 months, and Microsoft’s broader Work Trend Index framing shows the country moving quickly toward “frontier firm” behavior.

North America remains the largest geography in the category, while BCC Research says it is still the dominant regional market for AI agents. The regional contrast is important: North America has the biggest current base, while Asia-Pacific and India are the fastest-moving demand centers.

| Region / organization scope | Figure | Primary signal | Source |

| United States executives | 88% plan to increase AI budgets | Budget expansion | PwC |

| Indian business leaders | 93% plan to use AI agents in 12–18 months | Workforce extension | Microsoft |

| North America | Largest share | Current market leadership | BCC Research |

| Asia-Pacific | Fastest-growing demand base | Enterprise spend growth | IDC / Microsoft coverage |

Industry Adoption Rates

According to data compiled by Digital Applied from S&P Global Market Intelligence and McKinsey research, 31% of enterprises now have at least one AI agent running in production environments. However, adoption levels vary considerably by industry.

Financial services organizations are leading the market, while highly regulated sectors such as healthcare and government continue to move more cautiously due to compliance, security, and governance requirements.

AI Agents Production Adoption by Industry

| Industry | Production Adoption Rate |

| Banking & Insurance | 47% |

| Healthcare | 18% |

| Government | 14% |

The gap between banking and healthcare is particularly notable. At 47%, banking and insurance organizations are more than twice as likely as healthcare providers to have AI agents deployed in production environments.

Several factors explain this disparity:

- Banking and insurance firms have long invested in workflow automation, fraud detection, customer service automation, and data-driven decision-making, making them natural early adopters of agentic AI.

- Healthcare organizations face stricter regulatory requirements around patient data, privacy, and clinical decision support, slowing production deployment despite strong interest in AI-powered workflows.

- Government agencies continue to evaluate AI agents carefully because of public-sector procurement processes, security requirements, and accountability concerns.

The data suggests that enterprise AI adoption is entering a new phase where competitive advantage will depend less on experimentation and more on successful production deployment.

Industries with mature governance frameworks and well-structured data environments appear best positioned to capture value from agentic AI at scale.

5. AI Agents ROI & Productivity Statistics

This is the biggest tension in the market. Anthropic says 80% of organizations report measurable economic returns from AI agents, but WRITER says only 23% report significant ROI from AI agents specifically. That gap is what makes the category both exciting and under-optimized.

The productivity numbers are much stronger than the organizational ROI numbers. WRITER says AI super-users deliver 5x productivity gains, and Anthropic’s research says employees self-report using Claude in 60% of their work while reporting a 50% productivity boost. PwC also says 66% of organizations adopting AI agents say they are seeing measurable productivity gains.

At the macro level, the value story is large enough to matter even if ROI is uneven. Anthropic’s productivity research says AI can speed some tasks by 80%, which helps explain why executives keep investing even when enterprise-wide returns lag.

| ROI / productivity metric | Figure | Source |

| Measurable economic returns | 80% | Anthropic |

| Significant ROI from AI agents | 23% | WRITER |

| Measurable productivity gains | 66% | PwC |

| AI super-user productivity lift | 5x | WRITER |

| Claude used across work | 60% of work | Anthropic |

| Self-reported productivity boost | 50% | Anthropic |

| Task speed-up in Anthropic research | 80% | Anthropic |

6. AI Agents Governance, Risk & Security Statistics

Governance is now a core adoption metric, not a side issue. WRITER says 67% of executives believe their company has already suffered a data leak or breach due to unapproved AI tools, 36% have no formal plan for supervising AI agents, and 35% say they could not immediately pull the plug on a rogue agent.

Anthropic’s 2026 report points to a different kind of bottleneck: 46% cite integration with existing systems, 42% cite data access and quality, and 39% cite implementation cost. That means the blocker is not just model quality; it is operational plumbing and control.

The business consequence is simple. If Gartner is right that 40%+ of agentic AI projects will be scrapped by 2027, then governance failure is a direct financial risk, not an abstract compliance issue.

| Governance maturity / blocker | Share | Source |

| Data leak or breach from unapproved tools | 67% | WRITER |

| No formal supervision plan | 36% | WRITER |

| Cannot immediately shut down a rogue agent | 35% | WRITER |

| Integration blocker | 46% | Anthropic |

| Data quality blocker | 42% | Anthropic |

| Implementation cost blocker | 39% | Anthropic |

7. AI Coding Agents Statistics

Coding is one of the clearest proof points for agents. Anthropic says 89% of surveyed technical leaders use AI for coding, and Microsoft says 15 million developers are already using GitHub Copilot. That makes coding the most visibly mainstream agent workflow in the enterprise stack.

The workflow shift is also becoming structural. Anthropic’s coding trends report says engineers use AI in roughly 60% of their work, while Microsoft says GitHub Copilot adoption is already large enough to affect code review, deployment, and troubleshooting habits across teams.

That is why coding agents matter for backlinks and for product strategy: they are already moving from “assistant” to “production workflow layer.”

Read our complete breakdown of AI coding statistics here →

| Coding agent tool / signal | Reported metric |

| AI used for coding | 89% |

| GitHub Copilot developers | 15 million |

| AI-driven productivity boost | 50% self-reported in Anthropic work study |

8. AI Agents Regional & Geographic Statistics

The regional split is becoming clearer. North America is still the largest market by share, but Asia-Pacific is where the spending curve looks steepest. IDC says AI and GenAI investment in APAC should reach $175 billion by 2028, and GenAI spending in the region is forecast to grow at 59.2% CAGR.

India is the sharpest single-country acceleration signal. Microsoft says 93% of Indian business leaders plan to use AI agents within 12–18 months, which places India near the center of enterprise agent adoption conversations in 2026.

Anthropic’s geographic usage data also shows why region matters. In its 2026 Economic Index, the top 20 countries account for 48% of per-capita usage, and the top five U.S. states accounted for 24% of usage, down from 30% previously. That suggests adoption is spreading, but not evenly.

| Region | Market share / spend | Fastest-growing segment | Source |

| North America | Largest share | Enterprise deployment base | BCC Research |

| Asia-Pacific | $175B by 2028 | 59.2% CAGR for GenAI spend | IDC |

| India | 93% plan to use agents | Workforce extension | Microsoft |

| Global usage concentration | 48% from top 20 countries | Adoption remains uneven | Anthropic |

9. AI Agents Market Trends & Future Outlook Statistics

The defining trend in 2026 is the shift from single-task agents to multi-step, multi-agent systems. Anthropic says 57% of organizations already use agents for multi-stage workflows, and its coding trends report explicitly predicts that multi-agent systems will replace single-agent workflows in more advanced environments.

This shift is also changing how software is tested and validated. Instead of automating individual test cases, organizations are increasingly exploring AI-powered testing platforms that can generate tests from natural language, adapt to UI changes, and execute complex end-to-end workflows autonomously.

Platforms like Panto AI reflect this broader move toward agentic software quality, where AI helps create, maintain, and optimize testing processes rather than simply executing predefined scripts.

The next scale jump is already visible in forecasts. Microsoft cites IDC’s estimate of 1.3 billion AI agents by 2028, while Gartner says 33% of enterprise software applications will incorporate agentic AI by 2028 and 15% of day-to-day business decisions will be made autonomously.

That means the market is no longer asking whether agents will matter. It is asking which companies can govern them, integrate them, and prove value before budgets tighten and projects get canceled.

| Outlook signal | Figure | Source |

| Agents by 2028 | 1.3 billion | Microsoft / IDC |

| Enterprise software apps with agentic AI by 2028 | 33% | Gartner via Reuters |

| Day-to-day decisions made autonomously by 2028 | 15% | Gartner via Reuters |

| Multi-stage workflow usage | 57% | Anthropic |

| Project cancellation risk | 40%+ by 2027 | Gartner via Reuters |

Conclusion

The 2026 data makes one thing clear: the adoption debate is over. The question now is whether organizations can operationalize agents fast enough to justify the budgets they have already committed.

AI agent statistics in 2026 point to the same pattern from every angle: adoption is real, production is growing, and budgets are rising. The strongest headline numbers are 97% of executives saying their company deployed agents, 80% of organizations reporting measurable returns, and 51% already in production.

The bigger story is the gap between enthusiasm and control. With 40%+ project cancellation risk by 2027, 36% of organizations lacking a formal supervision plan, and 42% citing data quality as a blocker, 2026 is shaping up as the year the market separates vendors that can scale safely from those that can only demo well.

FAQ’s

Q: How big is the AI agent market in 2026?

A: The AI agent market is growing rapidly. Based on MarketsandMarkets’ published forecasts, the market is projected to reach approximately $11.5 billion in 2026, up from $7.8 billion in 2025. Other research firms estimate even larger market sizes due to broader definitions that include adjacent AI automation and infrastructure categories.

Q: What percentage of enterprises are using AI agents?

A: Enterprise adoption is already widespread, though deployment maturity varies. PwC reports that 79% of companies are adopting AI agents, while WRITER found that 97% of executives deployed AI agents during the past year. However, LangChain’s research suggests that only 51% of organizations have agents running in production, indicating that many deployments are still in early stages.

Q: What is the ROI of AI agents?

A: Most organizations report measurable value from AI agents, but results vary significantly. Anthropic found that 80% of organizations achieved economic benefits from AI adoption, while WRITER reported that only 23% have realized significant ROI specifically from AI agents. The gap highlights a common pattern: productivity gains often arrive quickly, while enterprise-wide transformation takes longer to materialize.

Q: What are the most common AI agent use cases?

A: The most widely adopted AI agent use cases center on knowledge work and process automation. LangChain reports research and summarization (58%), personal productivity (53.5%), and customer service (45.8%) as the leading categories. Anthropic’s data also highlights data analysis and report generation (60%) and internal process automation (48%) as major enterprise applications.

Q: What are the biggest challenges in deploying AI agents?

A: Security, governance, and data readiness remain the primary barriers. WRITER found that 67% of executives worry their organization has experienced a breach related to unauthorized AI usage, while 36% lack a formal AI governance framework. Anthropic’s research also identified system integration (46%) and data quality issues (42%) as major obstacles to successful deployment.

Q: How many AI agents will exist by 2028?

A: According to IDC projections cited by Microsoft, there could be approximately 1.3 billion AI agents in operation by 2028. While forecasts vary, this has become one of the most frequently referenced indicators of the scale expected for the agent economy over the next several years.

Q: Which industries are leading AI agent adoption?

A: Software development is currently one of the strongest adoption categories, with 59% of organizations using AI agents for coding, testing, debugging, or documentation workflows. Other leading sectors include data analysis and reporting (60%) and customer service (45.8%), reflecting the fact that AI agents deliver the greatest value in high-volume digital workflows with repeatable processes.