Shipping a fintech app is not like shipping any other product. Every release touches real money, real identity data, and real regulatory obligations.

This is the environment in which fintech teams have to move fast, and it is exactly why automated testing for fintech apps has become a foundational part of how serious teams ship.

The good news is that fintech application testing has become significantly more accessible over the last few years. You no longer need a dedicated QA team, a six-month framework setup, or a choice between release speed and product confidence.

This guide covers, from the five flows every fintech app should automate first, to the tooling decisions that make sense at each stage of growth.

Why Automated Testing for Fintech Apps Is Non-Negotiable

Fintech apps handle real money, real identities, and real trust. A broken payment flow is not just a bug, it becomes a churn event, a support ticket, and sometimes a compliance incident all at once.

This is why automated testing for fintech apps is not optional for teams that want to ship fast without breaking things that matter.

Most early-stage fintech teams know they need better testing. The challenge is that traditional approaches, including manual regression, record-and-playback tools, and enterprise-grade frameworks, were built for different contexts.

They were not designed for startups shipping every two weeks with two engineers, handling live money movement and regulatory exposure from day one.

The Cost of Inadequate Testing Is Higher in Fintech

In most app categories, a bug means a bad user experience. In fintech, a bug means something else entirely.

A failed payment confirmation can trigger a duplicate charge dispute. A broken KYC step drops a user mid-onboarding and costs you the activation permanently. A session management flaw can expose another user’s account data. That is not a UX issue. It is a regulatory one.

Fintech apps carry a unique combination of constraints that makes fintech application testing more consequential and more complex than testing in most other domains:

| Challenge | Why It Matters for Fintech |

| Zero failure tolerance | A broken Confirm Transfer screen is a regulatory incident, not just a UX bug |

| Device-dependent features | Biometrics, camera KYC, and OTP delivery require real hardware, not emulators |

| Compliance documentation | PCI DSS and SOC 2 require reproducible, auditable test records |

| Fast release cycles | Shipping every 1 to 2 weeks means manual regression is not a viable option |

| Device fragmentation | In markets like India, a large share of users are on older Android OEM hardware |

Each of these constraints raises the cost of inadequate coverage and makes structured automated testing for fintech apps more urgent the earlier you build it.

Why Manual Testing Breaks Down

Manual QA is not inherently bad. It is strategically limited for fintech teams that ship frequently. The core problem is that manual regression does not scale with release cadence.

If your team ships every two weeks and regression across your five critical flows takes three days of manual effort, you are spending roughly 30 percent of every sprint just verifying what already worked. That is not a testing strategy. It is a bottleneck.

Manual testing also has a coverage ceiling. A tester can only run so many device and OS combinations before the release window closes.

Payment behavior on a Redmi Note 8 running Android 10 with aggressive battery optimization may never get checked, even though a meaningful share of your users are on exactly that device.

Why Legacy Automation Tools Also Fall Short

Traditional automation frameworks solve the speed problem but introduce their own costs for lean fintech teams.

The maintenance trap. Tools like Appium are powerful, but they depend on element selectors, which are unique identifiers tied to specific UI elements. When a designer moves a button or renames a field, the selectors break.

Someone has to find every broken test, fix the identifiers, and re-run the suite. On a two-week sprint cycle, that someone is typically a developer pulled away from other priorities.

The brittle recording problem. Record-and-playback tools feel fast at first. You record yourself using the app and the tool generates a test.

But the recording captures exact pixel positions and element IDs at that moment. One UI update later, the test fails and has to be re-recorded from scratch.

The end result is predictable. Most fintech startups either skip automation entirely or maintain a set of tests that are always slightly broken, quietly misleading the team about what is actually covered.

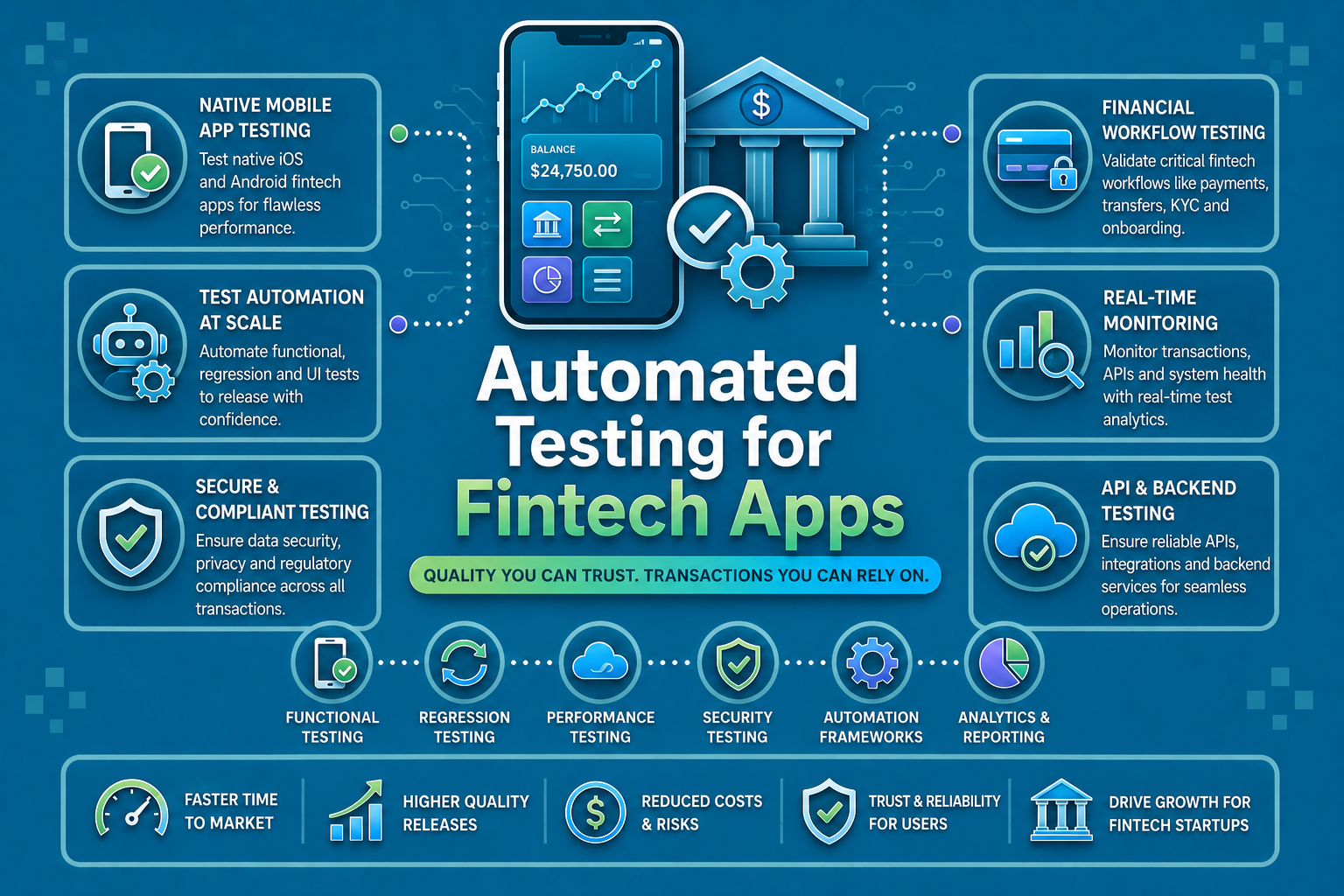

What Fintech Application Testing Covers

Fintech application testing is broader than checking whether screens load correctly. It spans security, compliance, device behavior, financial logic, and edge cases that only surface under real-world conditions.

The goal of thorough fintech application testing is to verify that your app behaves correctly for every user, on every relevant device, across every state of connectivity, and in every failure scenario that could expose the user to financial or data risk.

The highest-stakes areas fall into five categories, and those are the ones every fintech team should automate first.

The Five Flows to Automate First in Fintech Application Testing

Not everything needs to be automated on day one. Start with the flows where a failure directly harms users or triggers compliance risk. Everything else can be added incrementally once the foundation is stable.

1. Authentication and Session Management

Authentication is the gateway to every sensitive action in a fintech app. Failures here are not just frustrating. They are security incidents.

What to test in this flow:

- Biometric login including Face ID and fingerprint across iOS and Android versions

- PIN and password fallback for devices where biometrics fail

- Session timeout behavior: does the app save state mid-transaction before logging the user out?

- Re-authentication flow: can the user continue where they left off without losing progress?

- Concurrent session handling: what happens when the same account logs in on two devices simultaneously?

A biometric flow that works on iOS 17 may fail silently on Android 12 on a specific OEM device. Fintech application testing for authentication must run on actual hardware across your target device matrix, not just emulators.

2. Payment and Transfer Flows

This is the highest-stakes flow in any fintech app. A failure here is not recoverable with a UX fix.

What to test in this flow:

- Full end-to-end coverage: initiation, amount entry, payee selection, confirmation, processing state, and success confirmation

- Transaction record accuracy in history after completion

- Failure states: declined cards, insufficient funds, duplicate transaction detection, and timeout during processing

- Network interruption mid-transfer: does the app handle partial completion gracefully, or does it leave the user uncertain about whether the money moved?

- Edge amounts: minimum transfer thresholds, maximum limits, and decimal handling

Test failure states with the same rigor as success states. Users remember how an app handles failure far longer than they remember smooth transactions. In regulated markets, how you handle and communicate failures is itself a compliance matter.

3. KYC and Onboarding

KYC is where your highest drop-off rates live. A broken step in onboarding is a direct hit to activation, not just a bug report.

What to test in this flow:

- Camera access and document capture across device types and camera quality levels

- OCR validation accuracy on real document scans under variable lighting

- Liveness detection performance under different lighting and angle conditions

- Fallback flow for users whose documents fail the first scan: can they retry without restarting the entire process?

- Step-by-step progression without data loss on back navigation

- Re-entry flow: if a user exits mid-onboarding and returns, do they resume from the correct point?

KYC testing in fintech apps requires real devices specifically because camera behavior, processing power, and sensor quality vary significantly across hardware. Emulators cannot replicate this accurately, and it can only be automated on real devices.

4. Notifications and OTP Delivery

OTP and push notification behavior sits at the intersection of security and user experience. Failures here are invisible during internal testing but highly visible to users.

What to test in this flow:

- Push notification receipt in foreground, background, and Do Not Disturb states

- OTP arrival time across device types and carriers

- OTP timeout handling and the resend flow: does the old code expire correctly when a new one is requested?

- Notification behavior when the app has been force-closed or cleared from recent apps

- Deep link behavior: does tapping a notification route the user to the correct screen with context intact?

An OTP that arrives 45 seconds late makes the app feel broken even if every line of code is correct. Automated testing for fintech apps must include notification delivery as a first-class test case, not an afterthought.

5. Error States and Edge Cases

These are the scenarios users encounter least often and remember longest when they go wrong.

What to test in this flow:

- Invalid input handling: special characters, out-of-range amounts, and empty required fields

- API timeout behavior at each step of a critical flow

- Low-connectivity scenarios: 2G simulation, network drop mid-session, and reconnection handling

- Concurrent session conflicts

- Low-memory device behavior on older Android hardware

- Graceful degradation when a third-party service such as a payment gateway or identity provider is unavailable

Error state coverage is where fintech application testing separates teams that have already experienced production incidents from teams that are about to.

Building a Practical Device Test Matrix for Fintech Apps

A test matrix does not need to cover every device on the market. It needs to cover your actual users.

How to build yours:

- Pull your analytics and identify the top five device models and top three OS versions by active user count

- Add one to two older Android devices that represent your long-tail user base, especially in price-sensitive markets

- Include at least one iOS device on the latest OS and one on a version behind

- Run your critical flows against that matrix before every release

- Expand the matrix incrementally as your team and user base grow

A focused matrix of 8 to 10 device and OS combinations, executed consistently, gives you more production confidence than a sprawling matrix run once a quarter. Coverage discipline matters more than coverage breadth at early stages.

Why Real Devices Are Non-Negotiable in Fintech Application Testing

Emulators are fast and cheap. They are also insufficient for production-confidence testing in fintech. Here is what does not work reliably on emulators:

- Biometric authentication. Face ID and fingerprint require actual hardware sensors.

- Camera-based KYC. Document capture quality varies significantly across real device cameras.

- OTP delivery. Real SMS infrastructure and notification behavior cannot be replicated on emulated hardware.

- NFC payments. These require physical NFC chipsets.

- OEM-specific quirks. Background process handling, memory management, and battery optimization differ across Android manufacturers in ways that only surface on real devices.

For fintech application testing to reflect what users actually experience, it must run on real hardware. This is not a preference. It is a requirement for any flow that touches money, identity, or authentication.

How to Structure Automated Testing Into Your Release Cycle

Connecting Tests to Your CI/CD Pipeline

A test suite that only runs when someone remembers to trigger it is not a safety net. It is a checklist item that gets skipped under pressure.

The goal of automated testing for fintech apps is a setup where every pull request triggers a regression run against your critical flows automatically, and failures block the merge before the code reaches production.

How this looks in practice:

- Developer opens a pull request

- CI pipeline triggers an automated test run on real devices

- Results post to Slack or your dashboard within minutes

- Failures with affected flows are flagged before review or merge

- Release proceeds only when critical flows pass

Connecting automated testing for fintech apps directly to your CI pipeline removes the possibility of a known failure shipping undetected. It also transforms QA from a periodic activity into a continuous one that runs in the background of every sprint.

Compatible CI/CD systems include GitHub Actions, GitLab CI, Bitrise, and Azure DevOps. The tooling setup should not require a dedicated DevOps specialist to configure or maintain.

Who Should Be Writing and Reviewing Tests

In most fintech startups, QA responsibility either falls to one specialist or gets distributed informally across developers. Neither model scales well.

A more sustainable approach treats test authoring as a shared responsibility across the team:

- Developers write and maintain tests for new features before they ship

- Product managers define acceptance criteria that map directly to test cases

- Founders review coverage against compliance requirements at key milestones

Modern automated testing tools have reduced the technical barrier to writing tests significantly. When a test case reads like a plain-English user flow rather than a selector-based script, more team members can contribute and more perspectives catch edge cases earlier.

Tooling Considerations for Fintech Application Testing

What to Look for in an Automated Testing Platform

Not all automated testing tools are equally suited to fintech application testing. The requirements are specific enough that the wrong choice costs more time than it saves.

- Real device execution. Any tool that relies entirely on emulators will miss the hardware-dependent failures that matter most in fintech: biometrics, camera KYC, OTP, and OEM-specific behavior. Look for platforms with real device cloud access built in.

- Deterministic test results. In fintech, a test that passes on Tuesday and fails on Thursday for no clear reason is worse than no test at all. It creates false confidence. Your automated testing platform must produce consistent, repeatable results across every run. This is a baseline requirement for compliance documentation.

- Maintainable tests. If your test suite breaks every time a designer moves a button, your team will stop trusting it. Platforms with self-healing capabilities, where the tool automatically adapts to UI changes rather than failing silently, reduce maintenance overhead significantly on fast-moving fintech products.

- Readable failure reports. When a test fails before a release, your team needs to understand immediately what broke and why. Failure reports that require parsing raw stack traces add friction exactly when you can least afford it. Look for platforms that explain failures in plain language.

- CI/CD integration. Automated testing for fintech apps only works as a safety net if it runs automatically on every code change. The platform must integrate with your existing pipeline without requiring specialist configuration.

A Note on AI-Assisted Testing Tools

One category of tooling worth understanding is AI-assisted testing platforms. Rather than requiring engineers to write and maintain selector-based scripts, these platforms allow teams to describe flows in natural language, execute them on real devices via an AI agent, and convert successful runs into deterministic test scripts.

The practical benefit for fintech teams is reduced maintenance overhead. When UI elements change, the platform can remap affected steps automatically rather than breaking the entire test.

This matters specifically for fintech startups where product updates are frequent and dedicated QA engineers are scarce.

The key requirement to verify with any AI-assisted tool is determinism. The actual test execution, once the flow is captured, must be script-based and repeatable rather than dependent on a live AI model making decisions during regression runs.

How Panto AI Supports Automated Testing for Fintech Apps

Panto AI is built specifically for mobile fintech application testing on real devices.

How the workflow runs:

- A developer or PM describes a user flow in natural language

- Panto’s AI agent navigates the live app on a real device, executing the flow step by step

- The successful execution is converted into a deterministic Appium or Maestro script

- The script runs identically on every subsequent regression run with no live AI model involved at execution time

- When the UI changes, Panto detects the mismatch, adapts the affected steps, and notifies the team

What makes Panto suited for fintech application testing specifically:

- Conclusive debugging reports. Each failure report explains what the test was attempting, exactly where it failed, and the most likely root cause in plain English. Founders and PMs can understand failures without parsing crash logs.

- Deterministic execution. Once a flow is captured, it produces consistent, auditable results on every run. This makes it suitable for compliance documentation and release approvals.

- Real device coverage. Panto runs on real device infrastructure, making it possible to test biometric authentication, KYC document capture, OTP delivery, and low-network scenarios under production-like conditions.

- Free plan for early-stage teams. Panto’s free plan includes 15 test flows and 50 minutes of real-device execution, which is enough to cover login, onboarding, payments, transaction history, and error handling before your next release.

- Low setup overhead. Natural language and no-code authoring, as well as self-healing automation mean lean fintech teams can achieve reliable regression coverage without dedicated automation engineers.

What Fintech Application Testing Looks Like at Each Stage of Growth

Testing requirements evolve as your product and team grow. Here is what a practical progression looks like:

| Stage | Coverage Goal | What to Prioritize |

| Pre-launch | 5 critical flows on 5 devices | Login, KYC, payment, OTP, error states |

| Post-launch (0 to 6 months) | 15 to 20 flows across a real device matrix | Expand failure states, add API-level checks |

| Series A | Full regression suite running in CI/CD | All critical flows automated, compliance documentation in place |

| Scale | Parallel runs on 50 or more devices | Device fragmentation coverage, performance testing |

The teams that build testing infrastructure early, before Series B, before regulatory scrutiny, and before a high-profile production failure, are the ones that scale with the foundation to support it.

Getting Started with Automated Testing for Fintech Apps

You do not need a dedicated QA team to start. You need a process and the discipline to follow it consistently.

Step 1: Identify your five most critical flows. For most fintech apps, these are login and session management, fund transfer end-to-end, KYC onboarding, transaction history accuracy, and one core error state. These are the flows where failure causes direct user harm or compliance risk.

Step 2: Automate those flows on real devices before your next release. Describing a flow and running it on real hardware should take minutes with a modern platform, not days. Connect results to Slack so the team sees failures before they ship, not after.

Step 3: Connect to your CI pipeline. Every pull request should trigger a regression run. Failures block the merge. This one change removes the possibility of a known failure shipping undetected.

Step 4: Expand coverage one sprint at a time. Once your critical flows are stable, add error states, edge cases, and secondary flows incrementally. Test coverage should grow with your product rather than being retrofitted after a production incident.

Automated Testing for Fintech Apps Is a Trust Infrastructure Decision

For fintech startups, QA is not primarily about catching bugs before users do, though that matters. It is about building the kind of demonstrable, documented reliability that users stake their money on and that regulators require before you can scale.

Fintech application testing no longer requires a dedicated QA team, months of framework setup, or choosing between shipping speed and product confidence. Modern automated testing has made it possible for lean teams to run production-grade regression coverage on real devices, integrated into CI, with failure reports that the whole team can act on.

Start with your five critical flows. Automate them on real devices. Ship with evidence, not hope.

Looking to implement automated testing for your fintech app? Try Panto AI free with 15 test flows and 50 minutes of real-device execution, no credit card required.

FAQ’s

Q: What is fintech application testing?

A: Fintech application testing validates that financial apps work reliably and securely across critical flows like payments, authentication, KYC, OTP delivery, and edge-case handling under real-device conditions.

Q: Why is automated testing important for fintech apps?

A: Automated testing helps fintech teams validate critical flows before every release, reducing the risk of payment failures, authentication bugs, compliance violations, and production regressions. Manual QA alone cannot keep pace with modern release cycles.

Q: What should fintech application testing cover first?

A: Start with the highest-risk user journeys: authentication and biometric login, end-to-end payments, KYC onboarding, OTP delivery, and failure scenarios like network drops or API timeouts.

Q: Do I need a dedicated QA team for fintech automation?

A: No. Modern AI-powered testing tools allow developers, founders, and product teams to create automated tests using plain English or visual workflows. The key investment is process and CI/CD integration rather than large manual QA teams.

Q: Why is real-device testing important for fintech apps?

A: Emulators cannot fully reproduce biometric authentication, camera-based KYC flows, SMS OTP delivery, or OEM-specific Android behavior. Real-device testing provides results that better reflect actual user conditions.

Q: How often should automated fintech tests run?

A: Critical tests should run on every pull request in CI/CD pipelines. Broader regression suites should run nightly and before every release to ensure no high-risk flow reaches production unvalidated.

Q: What compliance standards require documented fintech testing?

A: Standards like PCI DSS, SOC 2, RBI guidelines, and FCA guidance all expect documented testing and reproducible QA processes for applications handling payments, authentication, and sensitive financial data.